A member who intends to claim a deduction for his/her personal superannuation contributions must give to the superannuation fund’s trustees a valid notice in the approved form before lodging their income tax return for the year in which the contribution was made or the end of the income year following the income year in which the contribution was made. Moreover, it is required that the trustees must also issue an acknowledge receipt of the notice.

As stated, in order to give effect to the deduction, the notice must be valid. According to section 290.170(2)(c) of ITAA 1997, a notice will not be valid when at the time the member gives notice to the fund’s trustee:

- The member is no longer a member of the fund; or

- The trustee no longer holds the contributions; or

- The trustee has begun to pay a superannuation income stream based on whole or part of the contribution.

In TR 2010/1, the ATO’s view is that any superannuation income stream commenced from a superannuation interest is based ‘in whole or in part on’ a contribution made to that superannuation interest.

The following will illustrate the application of the Section 290.170(2)(c):

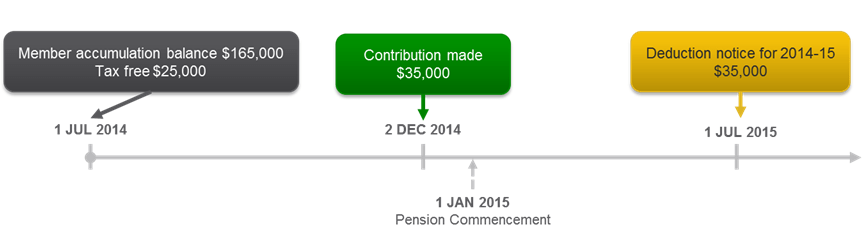

Paul has a superannuation interest valued at $165,000 at 1 July 2014. On 2 Dec 2014, he makes a $35,000 personal contribution so that his interest is valued at $200,000.

On 1 Jan 2015 he reached 65 years old and commences an account based pension using entire of his balance. However, the signed notice of concessional contribution of $35,000 and acknowledgement minutes provided for audit is dated 1 July 2015.

This notice Paul purports to give his fund to deduct the contribution will be invalid since at the time the notice was given (signed and dated 1 July 2015), the trustees have begun to pay a superannuation income stream based on the whole of the contribution.

Therefore, it is recommended that members should submit the correct signed deduction notice to the trustees before taking any action such as commencing a pension or withdrawing their benefits.