Members receiving a TRIS are able to access some superannuation benefits, without having to retire or leave their job, subject to 10% maximum withdrawals cap.

As a non-commutable income stream, there are certain restrictions on the circumstances in which the TRIS can be commuted.

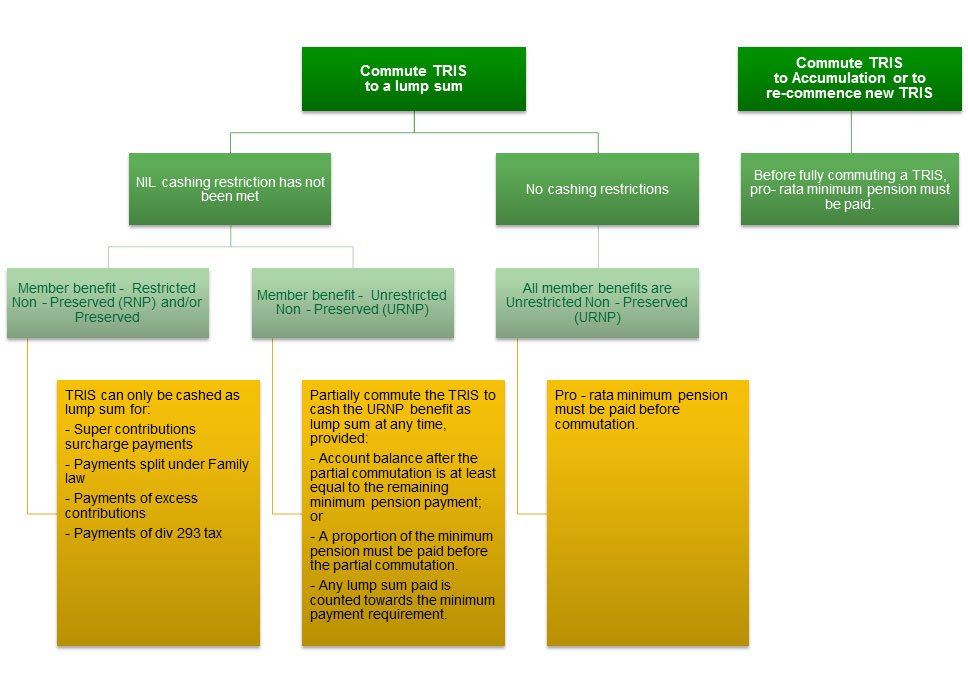

The following flowchart outlines the trips and traps advisers need to consider.

About the author

Naz Randeria is the Founder and Managing Director of Reliance Auditing Services. With more than 25 years’ experience in audit and accounting, Naz is an ASIC registered SMSF Auditor, SMSF Specialist Auditor, Registered Company Auditor, and Chartered Accountant.

She is actively involved in the SMSF audit sector and is passionate about sharing audit, compliance and SMSF knowledge with clients, professional colleagues and the wider public.

View Naz Randeria’s full profile