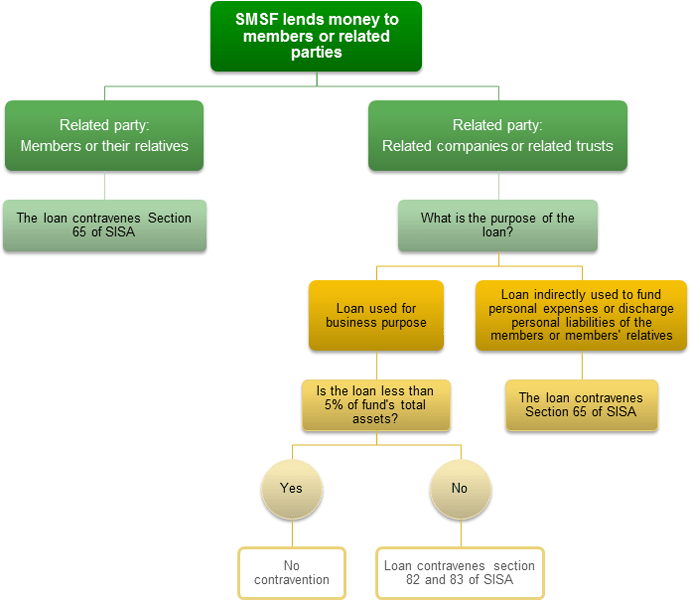

When a Self-Managed Super Fund (SMSF) lends money to members or their related parties, the loan constitutes as an in-house asset of the fund. However, it is not necessary that the fund has contravened Section 65 of the SIS legislation. The Australian Taxation Office (ATO) has provided an insight in SMSFR 2008/1 stating more factors need to be considered.

The flowchart below explains the workings of the SIS legislation.

Please click on image below to view larger version.

About the author

Naz Randeria is the Founder and Managing Director of Reliance Auditing Services. With more than 25 years’ experience in audit and accounting, Naz is an ASIC registered SMSF Auditor, SMSF Specialist Auditor, Registered Company Auditor, and Chartered Accountant.

She is actively involved in the SMSF audit sector and is passionate about sharing audit, compliance and SMSF knowledge with clients, professional colleagues and the wider public.

View Naz Randeria’s full profile