A superannuation fund is prohibited from purchasing assets from a related party except under certain circumstances. However, section 66 (2B) (b) (i) provides an exemption which allows a trustee to acquire assets from a related party in the event of a divorce or relationship breakdown.

A relationship breakdown in the SMSF environment can get complex when the parties go through the process of splitting and transferring of the assets from one spouse to another.

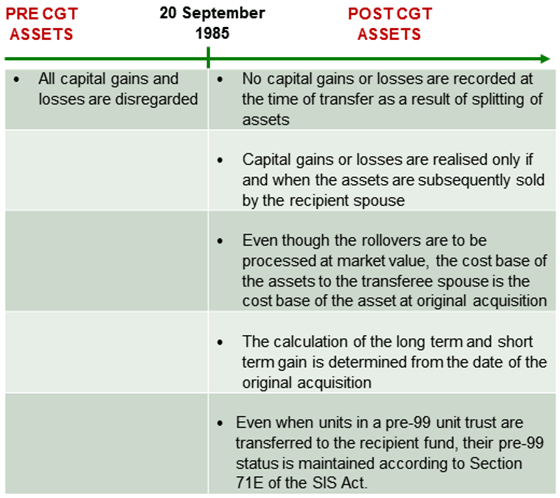

If assets are transferred as a result of a relationship breakdown, the rollover relief provisions specified in Section 126-140 of the ITAA 1997 can be applied. The rollover relief provisions ensure that the transferor spouse disregards a capital gain or capital loss that would otherwise arise. The recipient spouse pays tax only if and when the assets are subsequently sold at a later date.

It must be noted that the rollover relief provisions in Section 126-140 only apply as long as the receiving fund is a complying superannuation fund.

The following diagram is a simple representation of the rollover relief provisions.